About CREDITO

Credito is a decentralized credit analysis network that provides credit scores, transaction costs and credit markets supported by Ethereal, Intellectual and IPFS contracts, enhances transparency and reliability Introduction of the credit market is decentralized and provides links between creditors and borrowers living around the world. It removes physical barriers and reduces traditional borrowing and administrative costs. Visit https://credito.io/

CREDITO TOKEN CreDApp consults with CreditO

At that time, mandates were granted to maintain the Creator's risk profile and offer better interest rates for the network. If the creator wants to quickly fulfill the loan application, he can place an order with an earlier reduced interest rate.

Token network card

Credits include the ERC20 token, which functions as currency, management mechanism, and rewards system with Credito. Credito will be able to set prices and receive payments for its services in the form of loans - the use of markers. All Credito participants have to pay royalties on the use of the loan, which will be burned if it can increase the remaining loan demand, The total amount of loans burned in each transaction is directly proportional to the decrease in supply.

It also depends on the exchange rate set by the network, which monitors inventory, market conditions and exchange rates at any given time of payment. The fees for borrowers and lenders vary depending on the level of the transaction, we estimate the value of 0.5%. All three parties can integrate Credito Analytic Engine or from outside the Credito Credit Network for Banking to create credit risk by identifying future fraud transactions so that the industry can make informed decisions. Although financial institutions are widely recognized as one of the most regulated sectors, they remain scammers. The consequences of such fraud are insignificant, leading to financial catastrophes for banks and clients. Although financial institutions are actively involved in reducing the cost of fraud and fraud, they still lack the real global intelligence of all known fraud and compromise.

According to the Nilson Report in 2016, the loss of credit card cheats amounted to 2,015-2,8 billion dollars. The US, which is 162% more than the 2010 figure, which reached up to 8 billion US dollars. UNITED STATES OF AMERICA. Losses for 2016 are expected to reach more than $ 24 billion, and losses estimated at $ 31 billion by 2020.

The number of transactions with credit and debit cards by 2015 is $ 31 trillion. While the total value of credit card transactions grew by almost 7 percent per year, credit card fraud grew by more than 16 percent per year.

These losses occur throughout the system, including point of sale, ATM and online transactions. While EMV chip technology has reduced the frequency of in-store fraud, it does not help in online fraud.

Monopoly

Global credit intelligence is under the control of some credit bureaus, and it is often claimed that their scoring models are outdated, defective and not portable as they are specific to a country or region. "More than one in five consumers has a 'potentially significant error' in their credit history that puts them at risk of them, and consumers turn to one of the top three credit bureaus for information about the problem eight million times a year."

Security

Hack equifax recently revealed 140 million personalities and personal information to hackers and labeled as the worst security hole in US history In 2016, there were more than 15 million victims of identity theft or fraud, while the total stolen $ 16 billion.

Information center

Data collected by the central credit bureau. It is a common misconception that this agency automatically exchanges information, which is not true. This entity is a separate company offering similar services for a fee.

Portability

Because credit scores are non-transferable, low-risk borrowers may be denied access to credit when moving abroad because they are forced to recover their credit worthiness from scratch.

Obsolete analysis and incomplete information

As information becomes more centralized, monopolistic and incomplete. This leads to informed decisions available, which greatly increases the associated risk. In addition, credit scores are not updated in real time, and delays are set by millions of consumers and businesses because their current credit history is not taken into account in the decision-making process.

Credit Solutions

As a solution to the above problems, we only created Credito Network or Credito. Decentralized networks based on the Ethereal Block chain, combined with Intellectual Property and Interplanetary File Systems (IPFS), provide a decentralized credit and credit market. Credito promotes the work of a thriving and high-quality banking industry that enables financial institutions and digital resource loans to lend people and institutions backward or independent credit systems. The ecosystem provides solutions that enable trusted creditors to provide secure and secure loans to borrowers who are audited.

Credito design principles and values.

Decentralization.

Decentralization is not only the basis of protection against unauthorized access, but also for its infinite. By building a decentralized system, we want to expand conflict-free development within Credito. We believe that decentralization is an important component of a growing global ecosystem with long-term sustainability.

Modularity for simple and flexible systems.

We appreciate the philosophy of developing small tools that work well. Simple components are easy to put and can be integrated reliably into larger systems. We believe that modularity not only allows the modernization system, but also contributes to decentralization.

Safe, transparent and upgradable.

Credito built for the community. We appreciate the community and will continue to work with data researchers, experts, scientists and security experts to evaluate it. We ask for official tests, audits and safety proofs to create a platform whose reliability and safety can support future innovation.

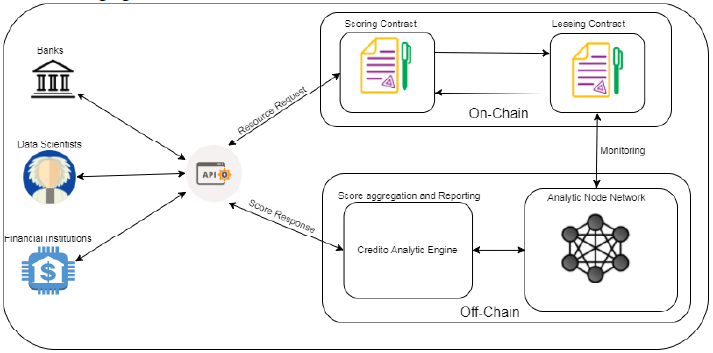

The election contract has two main tasks :

- Response to individual credit account requirements

- Review terms for third-party transaction calculations. In addition, loan balances and utilization rates are monitored.

For certain analysis nodes, leases control the following indicators :

- Number of queries specified: Number of requests approved for last node, completed and not executed.

- Total number of completed queries: Number of recent queries performed by node. This can be averaged based on the number of requests assigned to calculate the completion rate.

- Average response time: Timeliness of nodal response, which is an indicator of the effectiveness of the node. Average response time is calculated based on completed queries.

- Website reputation: A website's reputation based on previous transactions. All nodes check and print every point, and if most nodes return the same value, the node becomes reliable. This reputation system helps identify and remove the wrong websites from the network.

Credit - Online Credit Report

Loans are the ERC20 tokens used by Credito as the mechanism for fund management and rewards. Credito will be able to set prices and receive payments for its services in the form of loans.

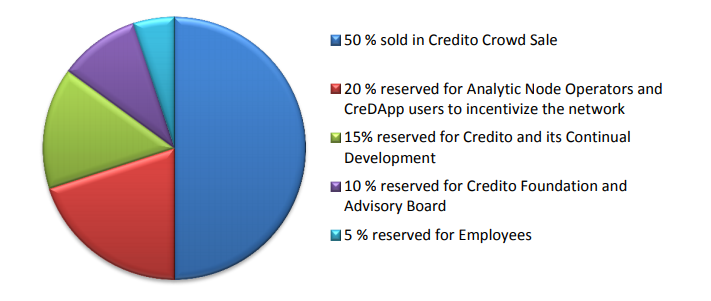

Token Distribution

In order to continue the development, Credito will perform a one-time "TGE" Sales and Sales Fee, with 50% of tokens available for public sale. The TGE start date will soon be announced and will provide a loan of US $ 1 billion. As follows :

- Employee distribution has a 12-month transition period, 25% - every quarter, with 6 months old rock. A proportional allocation to the ownership of each employee on the day the token is sold.

- With the distribution of Dana Credito, the transition period is 12 months.

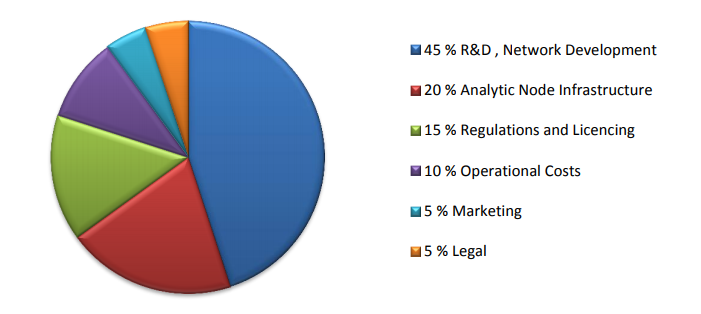

Use of funds provided

Roadmap

Credito will expand in 6 stages and set important milestones in each phase.

Stage1 is done

- Concepts and research.

- registry credit

- White paper

- The proof of this concept is a high-speed transaction system.

- Start a website

Registration, verification and partnership in the second phase

- CreDApp interface development

- user registration

- Automatic ID verification

- Work closely with financial institutions

Infrastructure and Intelligence Development Phase 3

- Development of external APIs.

- Infrastructure of analytical nodes.

- Development of credit development.

- Create a credit score.

- Model estimated transactions

Phase 4 Development and Dissemination of Intellectual Contracts

- Calculations and leases of intellectual contracts.

- Smart audit exams

- Integrated smart contract with Credito Analytic Engine and infrastructure node.

- Runs on the test network.

- Try a trial version, give your partner a direct result.

Stage 5 begins

- The main network starts.

- Decentralized intelligence controls are available for couples.

- External Analysis Node Operator that connects the network.

- Marketing and new partnerships.

The sixth stage protocol of end-to-end loans in large networks

- Develop CreDApp and Mobile App

- Development and audit of Smart Credit loan agreement

- CreDApp Brand with Credit Smart Credit Credit Integration

- CreDApp in the test network and the transition to the main network

Team

Advisors

PARTNERS

For more information :

- WEBSITE : https://credito.io/

- WHITE PAPER : https://credito.io/pdf/whitepaper.pdf

- FACEBOOK : https://www.facebook.com/CreditoNetwork

- TWITTER : https://twitter.com/CreditoNetwork

- TELEGRAM : https://t.me/CreditoCommunity

Penulis Artikel : Boyambon07

BitcoinTalk :

https://bitcointalk.org/index.php?action=profile;u=1505254

ETH : 0xE4Dcb7142A7fB9E3090059B69CedfEb88B2D2690

Tidak ada komentar:

Posting Komentar